What the US Stock Market Could Look Like From This Point Onwards

The US stock market is full of surprises, experiencing a meteoric rise of close to 30% in the S&P500 in 2021 alone, but falling 21% in the first half of 2022.

In the first 10 days of Aug 2022, the S&P500 showed tremendous potential by rising 5.2% to a four-month high. However, in the middle of the month, it changed course and rejected off a key resistance trend line, ending the month down 4.2%.

How will the US stock market perform from this point onwards? This article looks at some factors which could potentially drive the market, hopefully providing answers and clarity into the market.

Direction of the Federal Reserve (FED)

Comparing Today’s Economy to the 1970s

The US in the 1970s experienced a period of stagflation, combining high inflation with uneven and low economic growth. Some of the main causes included high budget deficits, low interest rates, oil embargos and the collapse of managed currency rates. Low interest rates fueled the high aggregate demand from consumers, while oil embargos limited the production and supply of oil, increasing transport and manufacturing costs.

Many economists believed that the FED policies in the 1970s, aimed at accepting higher inflation as its preferred alternative to a rise in unemployment, fostered damagingly high inflation expectations. This resulted in inflation so high that it required two recessions due to excessively high federal funds rate of 19% to bring the inflation rate down.

High inflation expectations is a self fulfilling prophecy. Consumers expecting prices to soar higher in the future would stock up daily necessities today, fueling the rise in aggregate demand, triggering higher inflation if the aggregate supply of goods in the economy is unable to keep up.

The US economy is currently experiencing high inflation, with the inflation rate year over year at 8.5% for the month of Jul 2022. This is most likely due to the low interest rates in 2020 and 2021 when COVID-19 first hit to stimulate the economy. The Russian-Ukraine war in 2022 also caused major supply chain disruptions, resulting in high commodities prices which contributes to high inflation.

Jerome Powell’s Jackson Hole Speech

On 26th Aug 2022, FED Chairman Jerome Powell mentioned that the Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back to the 2% goal. He hinted that aggressive interest rate hikes should be expected till the end of the year.

As the FED becomes more hawkish, consumers have lower inflation expectations due to the higher interest rate expectations.

This shows that the FED is effective in managing peoples’ expectations that the FED is committed to bringing down inflation, avoiding a similar situation in the 1970s where high inflation expectations continuously fueled higher inflation, to the point of requiring extreme rate hike measures. This meant that the FED does not need to hike interest rates too aggressively as long as people’s inflation expectations are kept in check.

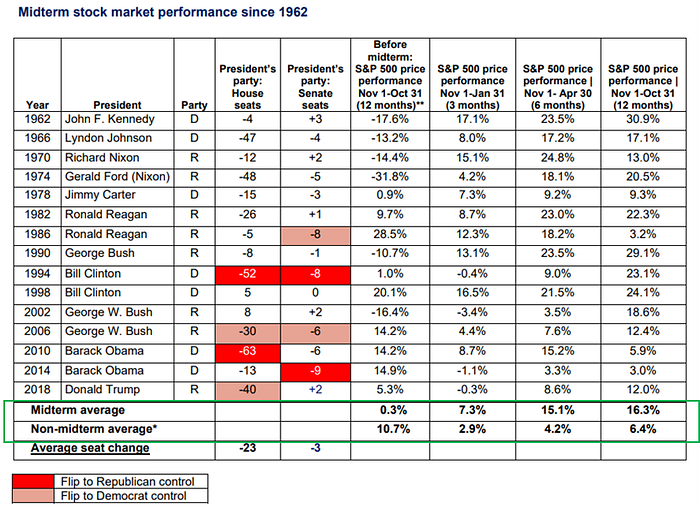

Midterm Elections

The average yearly returns of the S&P500 in the 12 months before a midterm election is 0.3% — significantly lower than those years without midterm elections at 10.7%.

On the other hand, the S&P500 performance after the midterm elections yield very different results. It has consistently outperformed the market in the 3-month, 6-month, and 12-month period after the midterm elections, compared to the years without midterm elections.

This contrast could be attributed to the fact that midterm elections pose some uncertainties in the US political scene. Such uncertainties may drive investors away, leading to the historically poor performance in the year leading up to the elections.

However, it is worth noting that negative pre-midterm market returns dominated the 1960s and 1970s, which was the era of stagflation in the US economy. If the five midterm elections in the 1960s and 1970s were to be excluded, the average S&P500 returns for pre-midterm election years were 8.1% —only slightly lower than the average annual S&P500 performance (8.5%).

This means that while midterm election years may be a factor driving US stock market performance, the overall macroeconomic conditions carry greater weight than any political uncertainty — which brings us to the next point.

Macroeconomic Conditions

Unemployment

While the unemployment rate is at its highest in six months, rising from 3.5% to 3.7% in Aug 2022, the participation rate jumped from 62.1% to 62.4%. This meant that more people entered the labor market in search of employment. Despite the rising unemployment, the labor market remains strong, showing that the US economy is not in a tight spot.

The rising unemployment rate is a concern if it continues. But the strong labor force gains we saw underneath are a really encouraging sign.

- Daniel Zhao, Lead Economist at Glassdoor

Inflation

The CPI increased for the past 12 months ending Jul 2022 by 8.5%, slightly lower than that ending Jun 2022 (9.1%). Even with the slight decrease in inflation rate from June to July, inflation rate is still at unprecedentedly high levels for the past 40 years, which is a bad sign for the economy.

However, the good news is that inflation expectations have been declining since April this year when the FED adopted a more hawkish stance. As mentioned earlier, this means that there is a possibility that the FED could keep inflation under control without increasing Fed Funds Rates too aggressively.

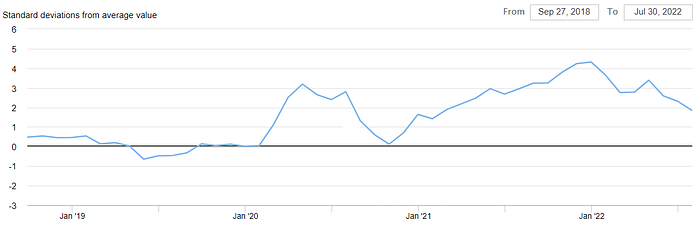

Global Supply Chain

Supply chain disruptions have been a major challenge since the start of COVID-19, mainly due to pandemic restrictions, safe management measures, and a surge in demand in online retail. The Russian-Ukraine War in Feb 2022 also caused some supply chain disruptions from the rapid rise in fuel prices.

The GSCPI above shows that supply chain pressures are at a downtrend since Jan 2022, which is a good sign for now. The ongoing Russian-Ukraine war may cause more supply-side issues, meaning that the GSCPI has to be further monitored to ensure it lowers down to pre-pandemic levels. If left unchecked, supply-side issues may cause inflation to reach higher levels.

Market Earnings/Valuations

Evidently, the incredible rise in stock prices in 2021 was fueled by the rapid rise in earnings. Most recent available data in Mar 2022 show that S&P500 earnings are still at very high levels, even though the stock prices do not justify it.

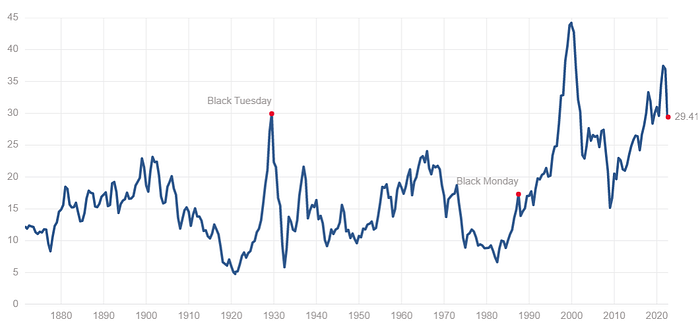

However, the Shiller P/E ratio, which is based on average inflation-adjusted earnings from the previous 10 years, shows that the S&P500 is currently overvalued. At 29.41 on 2nd Sep 2022, it is much higher than historical average values at 16.97, suggesting that stock prices still have much room to decline.

Overall Outlook

Considering the above factors, there are evidences which points to both directions which the stock market could head towards.

In my humble opinion, the US stock market would be volatile and bearish in the short run, from now till the midterm elections, which occurs in Nov 2022. In the long run, beyond Nov 2022, I believe that the absence of political uncertainties from the midterms elections and the evidences which point towards an improving economy would drive the US stock market to be bullish in 2023.

P.S. Disclaimer: Not Financial Advice